U.S. trailer demand defies spring slowdown

U.S. trailer demand strengthened again in April, with both FTR Intel and ACT Research reporting monthly and yearly improvements.

Net orders surged 11% month-over-month to 19,953 units—which is double FTR’s tally from April 2025—extending March’s upside surprise rather than entering the typical spring slowdown, FTR said. Orders also checked in well above the 10-year April average of 15,474 units, marking another constructive data point for a market that’s been under intense pressure.

U.S. trailer builds were essentially flat m/m in April, at 17,576 units, and up 1% y/y, FTR added. Calendar year-to-date builds also were roughly flat y/y, at 62,929 units, indicating continued production discipline among trailer manufacturers.

“Overall, the U.S. trailer market appears to be moving from deterioration toward stabilization and modest improvement,” Dan Moyer, FTR senior analyst for commercial vehicles, said in a news release. “Freight conditions are improving in pockets, but the recent rebound remains driven mainly by replacement demand and selective fleet activity rather than broad expansion. Trailers should therefore continue to lag Class 8 in the near term with improvement concentrated among stronger fleets, aged-equipment replacement, and dry van normalization.

“Cost and policy risks remain key overhangs and may already be shaping demand patterns. A change in how the Section 232 steel and aluminum tariffs are applied adds pricing and sourcing volatility for trailer equipment with significant metals exposure, and a van trailer antidumping and countervailing duties investigation adds further uncertainty.

“April trailer demand was better than expected, but a durable upcycle will likely require stronger fleet margins, higher trailer utilization, further absorption of excess capacity, and clearer visibility into trade-related costs.”

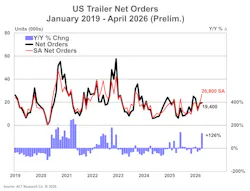

Order activity avoids typical decline

Preliminary net trailer orders hit 19,400 units in April, according to ACT data.

While that total was up only about 600 units from March’s 18,800-unit level, in a 3% m/m increase, it vaulted over a tepid April 2025 showing—improving by 126% y/y. Seasonal adjustment (SA) at this point in the annual order cycle takes the month’s volume to 26,800 units, ACT added.

“A sequential drop in net orders is typically expected, as April traditionally marks the second consecutive month of ‘weakest’ months of the annual order cycle,” said Jennifer McNealy, ACT director of CV market research and publications. “That said, this year’s cycle seems to have been delayed a few months, as the order upticks that should have started in September or October of last year didn’t actually happen until December. Regardless of the timing, the order upticks certainly are welcome.

“Given accelerating freight rates and rising carrier confidence, we raised the question last month about whether more high-side surprising order intake months would happen, or whether traditional Q2 order weakness would prevail as fleet decision-makers continue to hesitate about placing trailer orders while accelerating Class 8 tractor purchases instead in 2026. Based on the April data, we now know there was at least one more month of improved order intake in the pipeline, but it remains to be seen how the final two months of Q2 will unfold.

“Additionally, concern is mounting about how quickly trailer OEMs will build down the relatively still-thin backlog, particularly given concerns about the level of activity in the key freight-generating economic sectors that drive transportation demand and high petroleum prices that weigh on purchasing decisions for both consumers and fleets.”